Adrian Boulding: Seven ways to combat inflation in client portfolios

4th Nov 2022

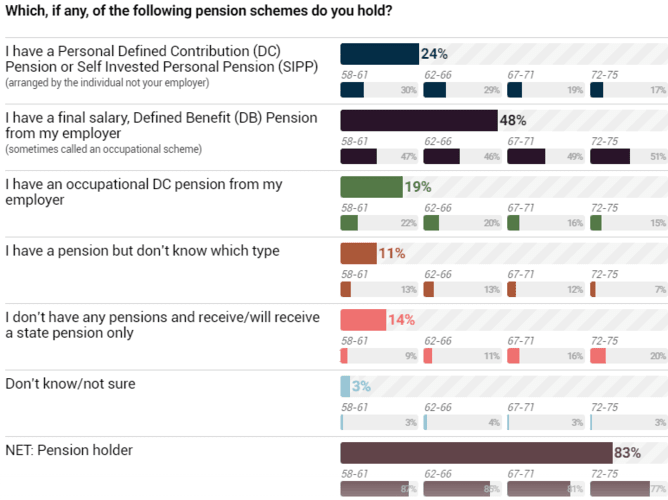

Approaching half (43%) of ‘baby-boomers’ – currently aged from 58 to 75 – are or will be reliant on defined contribution (DC) pensions for the bulk of their retirement income when they retire. The percentage of the soon-to-be-retired who are reliant on DC – rather than the more generous DB (defined benefit) pensions – is also close to the halfway tipping point.

Approaching half (43%) of ‘baby-boomers’ – currently aged from 58 to 75 – are or will be reliant on defined contribution (DC) pensions for the bulk of their retirement income when they retire. The percentage of the soon-to-be-retired who are reliant on DC – rather than the more generous DB (defined benefit) pensions – is also close to the halfway tipping point.

As an example, just 47% of the youngest tranche of boomers – aged 58 to 61 – which Dunstan Thomas contacted during a nationwide survey it commissioned earlier this year, had savings in a DB pension. Most of those DB schemes will have been closed for contributions many years ago. Furthermore, since pension freedom, annuity purchase at retirement has remained stubbornly low. In the 12 months to 31 March 2020, the FCA recorded that just 10% of the 673,831 who accessed their pensions for the first time bought an annuity.

As a result, protecting long-term savings earmarked for retirement from the twin effects of falling stock markets and high inflation has become a much higher priority for many more people approaching retirement and planning decumulation today.

For many, it may feel like it is too late to diversify if they have not done so already. After all, portfolios that were heavily exposed to equities have seen falls of between 20% and 30%, on average, in 2022 alone. That is a lot of value lost very quickly so would any action now not just be crystallising those heavy losses?

One strategy is to wait for markets to slowly recover their poise, and for inflation to begin falling. But when will that begin happening? Deutsche Bank has predicted UK CPI will not return close to the Bank of England inflation target of 2% until early 2025. Right now, inflation is still rising as we battle to restore the health of supply chains and keep a lid on rising energy prices amid the seemingly endless Russian conflict in Ukraine that continues to wreck a country’s infrastructure and cause untold human misery, while throttling Europe’s gas supplies.

Nevertheless, for anyone looking at diversification to tackle those twin destroyers of value – equity falls and inflation rises – here are seven options worth considering.

Inflation-linked bonds or ‘linkers’

In essence, this is investing in government debt and, as the name implies, the great benefit of these bonds is they rise with inflation. By buying a spread of 5-, 10- and 15-year bonds and holding them through to maturity, clients can choose a spread to match the dates they anticipate wanting their money out, secure in the knowledge the government will repay the stock at par on its maturity date, plus an uplift in line with the increase in the Retail Prices Index.

So called ‘linkers’ are often billed as the most trusted investment vehicle to hedge against inflation. An additional benefit of inflation-linked bonds is their returns do not automatically correlate with those of conventional stocks or other fixed-income assets as changes in their market value will reflect a combination of investors’ expectations of future interest rates and future inflation. Inflation-linked bonds also aid diversification to balance or rebalance portfolios.

Corporate inflation-linked bonds

Stepping away from government debt, we come to the inflation-linked national infrastructure debt market – notably utility sector linkers. One utility company currently active in the inflation-linked infrastructure debt market is Anglian Water. As a regulated utility company, it is allowed to raise its prices in line with inflation indices – making inflation-linked debt issuance particularly attractive.

Anglian Water’s debt also combines forward-looking environmental, social and governance (ESG) characteristics, as the company is actively raising capital to combat physical risks related to climate change.

It has set targets to help make the East of England more resilient to the risks of drought and flooding, for example. How borrowers address such environmental issues is now a fundamental part of credit assessment.

Currency hedging

It is also worth considering the impact of the weakening pound in terms of value destruction of UK-based stocks. What about investing in stocks listed in international stock exchanges in which inflation is lower and markets are steadier?

If inflation is going to be higher in the UK than in other countries, then conventional economic wisdom tells us the pound will continue to depreciate against other currencies, so that price comparison is maintained on international commodities. High inflation here inevitably makes it difficult for UK companies to maintain their profit margins as costs in their supply chain rise.

Anyone planning to move more funds into sectors that tend to do better in downturns anyway – most notably utilities, consumer staples, healthcare and technology firms enabling digital transformation – could consider selecting overseas stocks that are not listed on UK-based exchanges.

Residential property

Despite all the dire warnings of UK property market ‘corrections’ of up to 10%, there is a seemingly immoveable (over) demand versus (under) supply problem in the UK. Or, as Mark Twain put it: “Buy land, they aren’t making it anymore.” For the last 100 years we have witnessed a steady reduction in the size of the average household, as families become smaller and generations less likely to share. The problem of an under supply of land for development continues to play out in rising UK property prices.

Residential house prices increased by more than 10% in 2021 and just over 6% thus far in 2022. Next year, property prices are expected to surge by a further 5% despite the impact of higher mortgage rates. Property prices also tend to rise in periods of high inflation because the costs of labour and construction materials make construction less economically viable, further limiting new property supply, which as we know, is already a problem in the UK.

Property prices have strengthened in specific pockets of the market over the pandemic as many families chose to sell their homes in big cities, such as London, while using the balance to buy larger family homes in the country from which many chose to work from home. As a result, three-bedroom family homes with gardens and spare space to set up an office in rural or village locations have seen uplifts of between 15% and 20% during the pandemic. Two and three bedroom flats in London have also seen similarly outsized increases in value over the past two years. Have you also spotted fewer people attending Zoom meetings from their bedrooms? That bears witness to the growing trend towards larger properties.

Commercial property

The commercial property market is in the process of some reinvention – especially as demand for office space faces an uncertain future as the new hybrid working model persists. The lower-quality offices are probably the ones most at risk but it is possible to buy commercial property funds that specifically exclude office space – focusing instead on industrial, warehousing and retail units, for example.

For those who do not want to buy bricks and mortar outright but instead seek exposure to the sector’s growth, they can consider real estate investment trusts, which have historically performed well during periods of high inflation. Reits have the added advantage for would-be retirees of being a permissible investment in Sipps and SSASs. In addition, most commercial property leases worldwide are linked to one or other measure of inflation as well. So commercial rents often rise by the prevailing CPI or RPI rates of inflation.

Always be aware, however, of the ‘caps’ and ‘collars’ that can be built into commercial lease terms. It is not uncommon for leases to limit increases in so-called ‘ratchet clauses’ in commercial leaseholds – for example, in the long period of low inflation we have seen over the past 10 years or more, many leases set ratchet clauses to no higher than 5% per year. Now that CPI is running above 10%, however, that is not nearly sufficient.

Commodities

One major commodity that tends to hold value and at least keep pace with inflation is, of course, gold. Between 2016 and 2022, the gold price in US dollar terms nearly doubled to top out at $2,067 per ounce in August 2020 – though it is currently heading south. Silver may represent a less volatile play than gold as, in addition to its status as a precious metal, its price is underpinned by its many industrial and medical uses.

Investors can choose to buy unleveraged ‘physical gold’ exchange-traded funds (ETFs) that essentially invest in physical gold that is stored in a vault somewhere in a major city, such as New York or London, or they can buy ‘synthetic gold’ – essentially OTC (over the counter) derivatives based on gold.

Professional wisdom suggests buying into physical precious metal ETFs makes more sense right now because of the dangers of corrections in derivatives pricing associated with new commercial banking solvency rules bound into Basel 3 which will limit banks from increasing their exposure to derivatives further.

While investigating commodities, it is worth considering investment in some of the ‘rare earths’ that are finding increasing demand as we all transition over the next 10 years from driving around in internal combustion engine vehicles and move to electric ones. Electric vehicles (EVs) require batteries that themselves are built with lithium, cobalt, nickel, manganese, graphite and cerium ‘rare earths’, among others. It is possible to invest in a basket of ‘rare earths’, again through ETFs.

It is also worth considering the inevitable demand for copper as property owners upgrade the wiring in their homes and offices to enable the rapid charging of EVs, and eventually to move spare electricity from a vehicle or home electricity storage units into local microgrids, which will be established to trade locally produced power (from solar panels, windmills, air source and ground source heat pumps and so forth).

Going green

Finally, it may well be worth clients putting any cash savings – which are anyway losing value in a high-inflation economy – to work to invest in solar panels on their roof, now prices of photovoltaic panels have fallen. Others may consider buying shares in wind farms or even owning shares in wind turbines themselves. Energy, in its various forms, is a major component of the calculation of CPI inflation, so investing in energy could deliver a useful degree of inflation protection to a portfolio.

It is never wise to undertake a ‘big bang’ diversification away from existing holdings but it may be worth exploring some exposure to some of the above investments to hedge against the potential ravages of inflation, particularly as it looks like we will be in this high inflationary cycle for at least one more year before it starts to move down towards the lower rates we all grew used to for many years pre-pandemic. One thing is certain though, demand for investment advice was never higher than it is in these volatile, high inflationary times.

Dunstan Thomas Baby Boomers Report Previous Article

Adrian Boulding

Director of Retirement Strategy at Dunstan Thomas

023 9282 2254

info@dthomas.co.uk