Pension freedoms exposed a longevity problem we still refuse to confront

11 Mar 2026

First seen in Professional Adviser

First seen in Professional Adviser

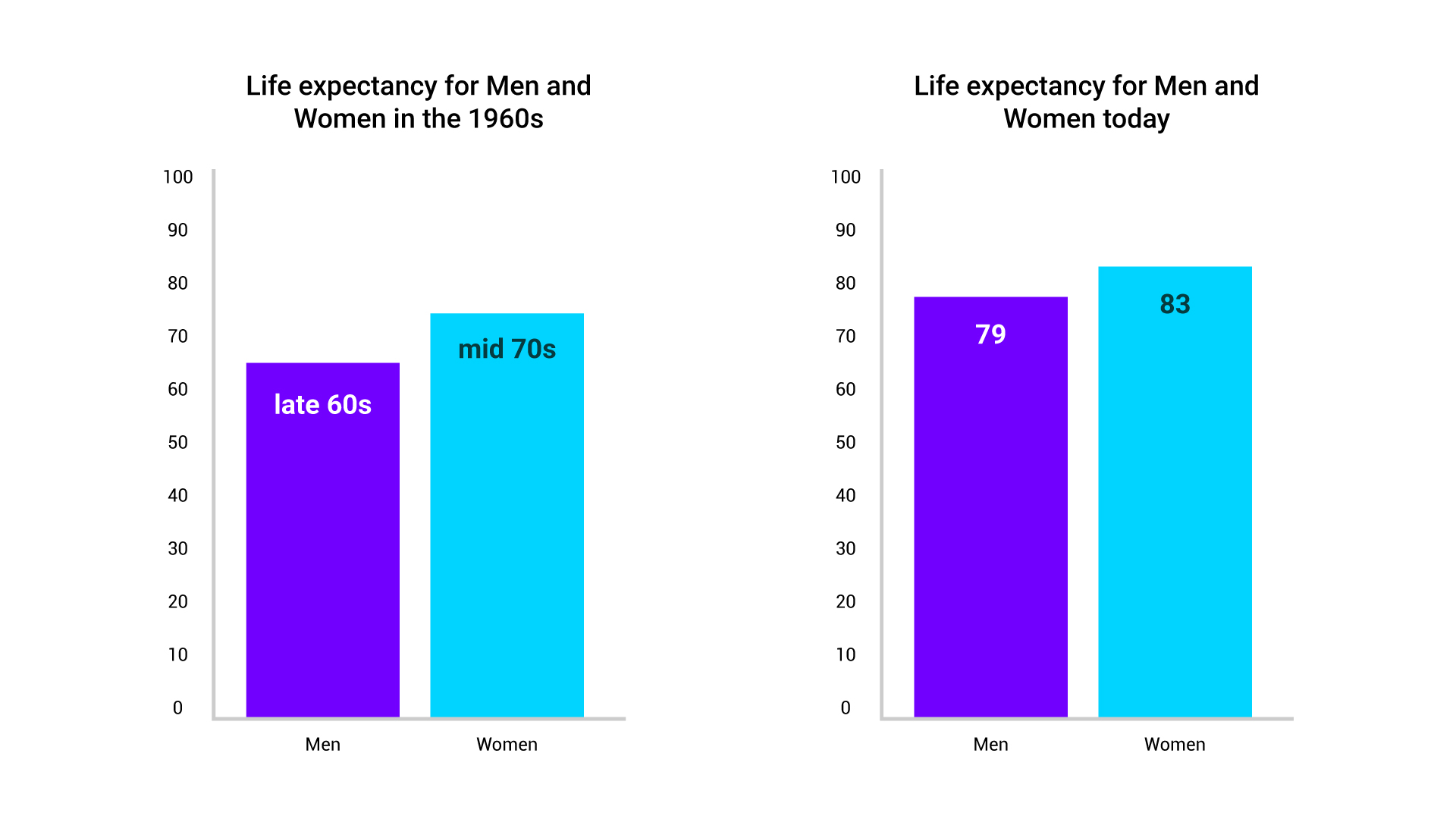

People are living longer than ever before. In the 1960s, for example, reaching 90 was relatively rare, with UK life expectancies somewhere around late 60s for men and mid-70s for women. Today, life expectancies are considerably longer, with men expected to live to around 79, and women 83. Reaching 90 is certainly no longer an unusual phenomenon.

When it comes to financing those extra years, however, longevity becomes a problem for the UK pensions system. Many people cannot, and will not, be able to financially support themselves throughout their later life.

The impact of pensions freedoms

The introduction of pension freedoms exposed this problem. By dismantling a largely predictable system of retirement income and replacing it with personal choice and personal risk, an extraordinary burden was placed on individuals to manage longevity, investment and behavioural risk for decades, maybe even 30 years or more. The new system assumed people would make informed, rational decisions or seek advice. Advice, however, was never mandatory. Pensions are complicated. People often do not make rational choices with their money, even if they believe they are doing the right thing.

For decades, longevity risk sat primarily with providers and insurers. Defined benefit schemes and annuities pooled risk across populations and time. The individual traded flexibility for certainty. Pension freedoms turned that on its head. Longevity risk now sits squarely with the saver, often without the tools, understanding or ongoing support needed to manage it.

The decline in annuities was an early signal. Low interest rates made them appear to be of poor value, but that was only part of the story; they also represented constraint in a system that suddenly celebrated choice. Drawdown, once a specialist product for the wealthy and advised, moved rapidly into the mainstream. Today it is no longer niche. It is the default pathway for many retirees, including those with modest pots and limited financial resilience.

Drawdown can work well. Used properly, it offers flexibility, tax efficiency and adaptability to changing circumstances. Used badly, it accelerates depletion. Sequence risk, over-optimistic withdrawal rates and poor market timing remain poorly understood outside professional circles. In addition to this, longevity assumptions are routinely understated - a healthy 65-year-old planning to live to 85 is not being ambitious; they are underestimating their lifespan.

This creates a mismatch that the industry has yet to resolve. We expect consumers to understand sustainable withdrawal rates, inflation risk, asset allocation and tax interactions, while presenting choices through interfaces optimised for accumulation rather than decumulation. The gap between product complexity and consumer understanding is not narrowing.

The macroeconomic impact of widespread under-saving and over-spending in retirement

The consequences extend beyond individual outcomes. Depleted pension pots feed directly into future fiscal pressure through housing support, healthcare costs and benefits. The macroeconomic impact of widespread under-saving and over-spending in retirement is rarely discussed with the seriousness it deserves. An ageing population drawing down assets faster than anticipated has implications for capital markets, intergenerational wealth and public finances.

It surely, then, cannot be a case of whether government intervenes, but how and when. A return to compulsion in some form is already being debated quietly – consider the Financial Conduct Authority’s work on default pathways, for example. The language may focus on consumer protection, but the underlying driver will be sustainability of personal capital for the long-term.

Technology has a role to play here, but only if it is deployed with intent rather than optimism. Intelligent guardrails can prevent catastrophic decisions without removing choice. Real-time sustainability modelling can show the consequences of withdrawals as they happen, not years later in an annual statement. Behavioural nudges, applied carefully, can encourage pacing rather than panic. Automated suitability checks can flag when drawdown is no longer appropriate and when risk is being taken unknowingly.

AI-enabled hybrid advice could play a role, offering a way to reintroduce structure without reinstating a one-size-fits-all system. Scalable guidance supported by human oversight can help close the advice gap that pension freedoms exposed but never addressed.

None of this removes personal choice. It does, however, reframe it within a system that acknowledges human behaviour, longevity uncertainty and the limits of financial literacy. Pension freedoms gave people control, but control without support risks poor long-term outcomes for today’s retirees.

For a population enjoying longer lives, we need long-term thinking in pensions. Future changes to the pensions system need to be grounded in realism about how people really behave in retirement, not how policy hoped they would.

Previous Article Contact UsJulia Fintz

Co-Managing Director at Dunstan Thomas

023 9282 2254

enquiries@dthomas.co.uk